|

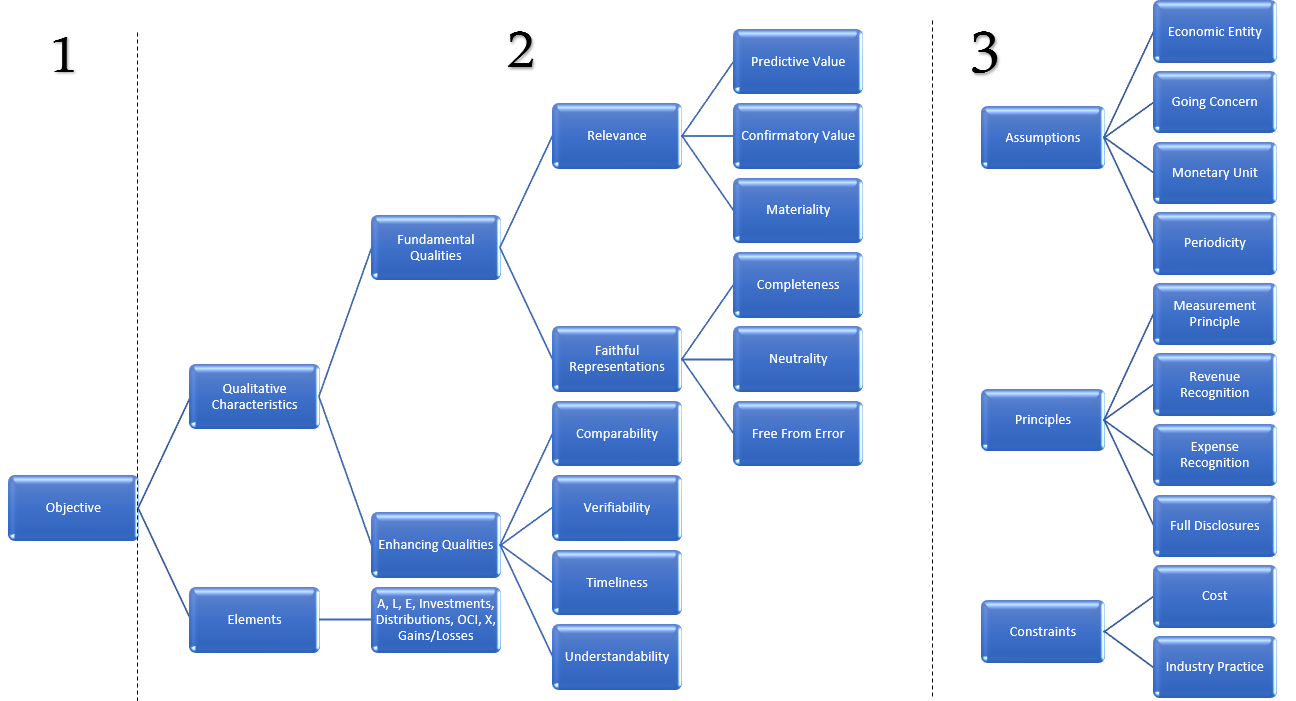

FASB’s Conceptual Framework establishes concepts of underlying financial reporting. There are three levels. Level 1: Objectives – providing information that is useful to present and potential equity investors, lenders, and creditors (underlying in their capacity as capital providers). Therefore, for financial reporting to be useful, it must provide the useful information for investment decisions. Level 2a: Qualitative Characteristics including Fundamental Qualities, and Enhancing Qualities Level 2aa: Fundamental Qualities includes relevance and faithful representation. Level 2aaa: Relevance is information helpful in making decision being Predictive Value, Confirmatory Value, and Materiality. Predictive Value – Relevant information used by investors to form their own expectations Confirmatory Value – Relevant information helping users confirm or correct prior expectations. Materiality – information is material if omitting (and or misstating) could influence decisions relying on the financial statements. Level 2aab: Faithful representation are that numbers and descriptions match exactly what happened, ensuring completeness, neutrality, and free from error. Completeness – refers to all information that is necessary for faithful representations is provided. Neutrality – is where a company cannot select information to favor one set of interest parties over another. Free from error – refers to more accurate faithful representation of a financial item. Level 2ab: Enhancing Qualities includes Comparability, Verifiability, Timeliness, and Understandability. Comparability – refers to information that is measured and reported in a similar manner considered comparable (CONSISTENCY). Verifiability – occurs when independent measurers, using same methods, obtaining similar results Timeliness – refers information available to decision-makers before it loses relevance, or capacity to influence decisions Understandability – refers to the quality of the information that lets reasonably informed users to see its significance. Level 2b: Elements – This includes assets, liabilities, equity, investments by owners, distributions to owners, comprehensive income, revenues, expenses, gains/losses. Level 3: Assumptions, Principles, and Constraints Level 3a: Assumptions inclusive of economic entity, going concern, monetary unit, and periodicity. Economic Entity – refers to a company that keeps its activity separate form its owners and other businesses Going Concern – refers to a company that last long enough to fulfill objectives and commitment Monetary Unit – refers to money as a common denominator Periodicity – refers to a company dividing economic activities into time periods Level 3b: Principles inclusive of Measurement, Revenue Recognition, Expense Recognition, and Full Disclosures. Measurement principle – refers to the most commonly used measurements that are based on historical costs and fair value Revenue Recognition – refers to the general occurrence when realized or realizable revenues are earned Expense Recognition – Letting the expenses following the revenues Full Disclosures – Providing information that is sufficient in influencing judgement and decisions for an informed user, inclusive of financial statements, notes to financial statements, and supplementary information. Level 3c: Constraints inclusive of Cost and Industry Practice Constrains Cost Constraint – refers to cost of providing information must be weighed against the benefits from using it Industry Practice Constraint – refers to the unique nature of an industry and business concerns sometimes that require any potential departure from accounting practice

0 Comments

Leave a Reply. |

Archives

June 2019

Categories |

RSS Feed

RSS Feed